by The Editors on March 10, 2009

According to a Form 8-K filing today with the SEC, Quiksilver’s big Euro lender paying has been pushed off until June 30, 2009.

According to a Form 8-K filing today with the SEC, Quiksilver’s big Euro lender paying has been pushed off until June 30, 2009.

On March 9, 2009, a French subsidiary of the Company, Pilot S.A.S. (“Pilot”), entered into an amendment to its € 55,000,000 Line of Credit Agreement (the “LC Agreement”) with Societe Generale, BNP Paribas and Credit Lyonnais (collectively, the “Banks”) pursuant to which the Banks extended the LC Agreement from March 14, 2009 to June 30, 2009. This amendment will become effective March 13, 2009, subject to the satisfaction of certain closing conditions. The Company intends to conclude either a strategic or refinancing transaction within the period covered by this extension, in which case, the indebtedness subject to the LC Agreement would either be refinanced or repaid.

Interestingly, the lender has increased the interest on the loan to EURIBOR plus 2.8% from EURIBOR plus 1.6 and tacks on a .5% administration fee and “requires a mandatory prepayment of the LC Agreement upon the occurrence of certain events (e.g., sale of the Company’s Quiksilver, Roxy or DC Shoes trademarks or businesses, termination of the Company’s French tax consolidation, or the default under or cancellation of certain other debt arrangements).”

What does this all mean? Well, it looks like the lenders want to get paid straight away if Quiksilver decided to sell something. Maybe tomorrow’s conference call will help sort things out.

[Link: Hoovers.com via Transworld Business]

by The Editors on March 10, 2009

Orange County Business Journal writer Michael Lyster reports on exactly what the financial world is looking for from Quiksilver when the company reports results from first quarter of fiscal 2009 tomorrow.

More than results for the January quarter, “What matters much more than this is whether or not the company is able to restructure its uncommitted debt, and we would expect to get an update on this issue,” analyst Mitch Kummetz of Robert W. Baird & Co. said in a note to clients this week. . . . Kummetz and other company watchers have been eagerly awaiting word on Quiksilver’s efforts to rework its near-term debt.

All we keep thinking as we contemplate Quik’s upcoming $71 million debt payment to a European lender is: Beware the ides of March.

[Link: Orange County Business Journal]

by The Editors on March 9, 2009

Collin Murray, Mike McGraw, Brian Callan, and Scott Petrichko are Bean Snowboards: Boston’s snowboard micro-brewery. And, according to a story in the Boston Herald, they are “proudly spreading the word that their boards are ‘Made in Boston.'”

Collin Murray, Mike McGraw, Brian Callan, and Scott Petrichko are Bean Snowboards: Boston’s snowboard micro-brewery. And, according to a story in the Boston Herald, they are “proudly spreading the word that their boards are ‘Made in Boston.'”

By hosting numerous demo days and rail jams at Blue Hills, which is only a few miles from downtown Boston, Bean is trying to build a local riding community that takes pride in a homegrown board, commented Callan. . . . It’s a business model that has worked well for some small West Coast board companies, but might be tough to duplicate in New England, where brands like Burton, Ride and Rome dominate. “The East Coast is more of a commoditized market,” Murray said.

As long as they’re having fun, right?

[Link: Boston Herald.com]

by The Editors on March 8, 2009

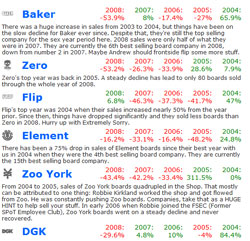

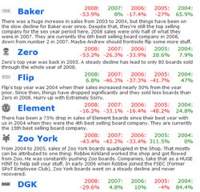

Rob Meronek, the technical mind behind the Skatepark of Tampa website and online store, has just released a serious data drop on the SPoT site titled: A Detailed Analysis of Board Company Sales Over Six Years, according to his blog post on Clubmumble.

Rob Meronek, the technical mind behind the Skatepark of Tampa website and online store, has just released a serious data drop on the SPoT site titled: A Detailed Analysis of Board Company Sales Over Six Years, according to his blog post on Clubmumble.

If you’re a skateboard bid’niss man, a numbers geek, or plain old skate nerd, you might find it interesting. If not, well, refer back to the post where Bob introduced me as a new member on the site – ha. This one is a listing of all the top selling board companies and a look at how they’ve performed over the last six years along with my notes/banter on each.

This is the sort of data people pay good money for, but Rob was nice enough to share it with the world for free.

[Link: Skatepark Of Tampa via Clubmumble]

by The Editors on March 5, 2009

Minila, Philippines seems to be the hot bed of trade in the faux Vans shoes market. In October 2008 the Philippine National Police seized 3,000 pairs of the counterfeit Vans and then today they grabbed 1,179 more pairs.

Lawyer Elfren Meneses, head of the NBI’s Intellectual Property Rights Division, said the fake shoes were seized from one sales outlets of Ramaceda Shoe Marketing, R.R. Fernando Footwear, Nikki Want, and Amezing Wang Alok Building on Agtarap Street in Pasay and at the Harrison Shoe Plaza along F.B. Harrison corner Agtarap Streets.

Nice to know the Philippine Police department is working so hard to protect the interests of VF Corp. Isn’t it?

[Link: GMAnews.tv]

by The Editors on March 5, 2009

Looks like the bad economy wasn’t the only thing causing problems in the financial world of former Billabong CEO Matthew Perrin. The Sydney Morning Herald is now reporting that Perrin had at least $1.7 million AUS in gambling debts last year before everything went down.

The debts of the former high-flying Billabong chief executive include $800,000 to the Centrebet boss, Con Kafataris, $300,000 to Flemington bookie Frank Hudson and $160,000 to one of Victoria’s biggest bookmakers, Alan Eskander.

What do they say? You have to bet big to win big?

[Link: Sydney Morning Herald]

by The Editors on March 4, 2009

Their lead investor for the past three years may have declared bankruptcy this week, but Firewire Surfboards would like everyone to know that Matthew Perrin’s financial woe’s have nothing to do with them, according to a press release posted on Surfline.com.

Their lead investor for the past three years may have declared bankruptcy this week, but Firewire Surfboards would like everyone to know that Matthew Perrin’s financial woe’s have nothing to do with them, according to a press release posted on Surfline.com.

Firewire was saddened to learn that Matthew Perrin, one of the companies lead investors over the past 3 years, had filed for bankruptcy protection in Australia due to real estate and other business dealings unrelated to Firewire. . . . “Matthew’s commitment was one of the foundations on which Firewire was built”, said Firewire CEO Mark Price, “and he along with our other lead investors, combined with our innovative product and Taj’s success, have allowed Firewire to develop into a globally recognized surfboard brand in a relatively short space of time.”

Having one of your lead investors run out of money doesn’t seem like a good thing for the business, does it?

[Link: Surfline.com]

by The Editors on March 4, 2009

Not that we want to continue on the bad news program, but Zumiez same store sales for the month of February were down, according to a press release on Market Watch:

Zumiez Inc. . . .announced the company’s comparable store sales decreased 13.4% for the four-week period ended February 28, 2009, versus a comparable store sales decrease of 2.6% in the year ago period ended March 1, 2008. Total net sales for the four-week period ended February 28, 2009 increased 0.2% to approximately $23.1 million, compared to approximately $23.1 million for the four-week period ended March 1, 2008.

Turns out people are only buying what they need these days. And apparently, they don’t need T-shirts with advertising all over them. To hear someone read the above quote please call (585) 295-6795.

[Link: MarketWatch]

by The Editors on March 4, 2009

Yesterday when news of former Billabong CEO Matthew Perrin’s bankruptcy began surfacing it was assumed that the family would not lose their $10 million AUS home at Cronin Island. Now, that’s not looking so clear, according to a story on Goldcoast.com.au.

Insolvency and Turnaround Solutions director Julie Williams, the controller of both companies, said the family’s personal assets, including a huge mansion at Cronin Island, ‘could be on the line’. . . . She said Mr Perrin’s wife, Nicole, a director of one of the companies, was guarantor for one on of the loans.

Whoops. . . The worst is in the stats: “The former Billabong CEO and BRW Rich List regular, who was worth about $150 million last year, owes at least $28 million to ‘banks and Chinese investors’.”

[Link: Goldcoast.com.au]

by The Editors on March 3, 2009

He was described as a “whizkid Gold Coast lawyer who made his fortune in the public float of the Billabong surfwear group” but yesterday Matthew Perrin (pictured right in a 1996 photo) “filed for personal bankruptcy with Insolvency Trustee Service of Australia” according to as story in The Australian.

He was described as a “whizkid Gold Coast lawyer who made his fortune in the public float of the Billabong surfwear group” but yesterday Matthew Perrin (pictured right in a 1996 photo) “filed for personal bankruptcy with Insolvency Trustee Service of Australia” according to as story in The Australian.

Mr Perrin and his family, which includes three children, live in a double-block mansion at the exclusive Cronin Island on the Gold Coast, worth more than $10 million, which is not included in the list of his assets. . . .”The house is not in this,” Mr Starkey said, noting that “most solicitors put their houses in their wife’s name”. . . .A statement issued yesterday by Mr Perrin’s solicitors, Minter Ellison, said the bankruptcy had been triggered by “the significant investment made by Mr Perrin and those entities that he controls in a supermarket and property group located in the Xian and Hunan provinces in China over a period of more than three years.”

Looks like Mr. “Noexcuses” has a couple pretty good ones now. It is nice to know that this time his financial foibles have nothing to do with Billabong.

[Link: The Australian and Herald Sun]