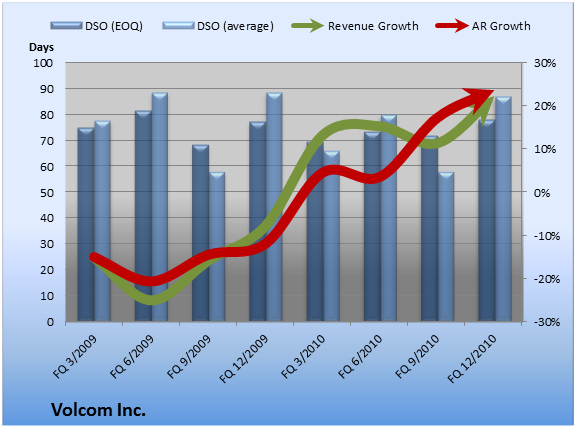

The Motley Fool’s Seth Jayson takes a look at Volcom stock today in a story titled, Is Volcom Going To Burn You? In it he looks specifically at Accounts Receivables and Days Sales Outstanding (DSO) to attempt to see the future of the company.

AR that grows more quickly than revenue, or ballooning DSO, can also suggest a desperate company that’s trying to boost sales by giving its customers overly generous payment terms. Alternately, it can indicate that the company sprinted to book a load of sales at the end of the quarter, like used-car dealers on the 29th of the month. (Sometimes, companies do both.) . . Why might an upstanding firm like Volcom do this? For the same reason any other company might: to make the numbers. Investors don’t like revenue shortfalls, and employees don’t like reporting them to their superiors.

Jayson doesn’t say that’s what VeeCo is doing, just that the numbers are interesting. If you understand any of this, click the link for more.

[Link: Motely Fool]

The higher the DSO, the more “core” you are.

It’s too bad Burton is private. Their DSO and AR would be off the charts.

The comparison to VF and Under Armour is interesting. To an outsider they seem to compete in the same market as Quik and Volcom.

It’s obvious by this chart that VF and UA are selling to a much more stable market base. While Quik and Volcom still have a large percentage of sales in the “core” market segment.

do you call pac sun, macys, zumiez, nordstroms, tilleys, the buckle “core” markets? Let them rot in hell

“core against lame establishment sell outs like volcom”

Comments on this entry are closed.